Automated Risk Assessment & Scoring

Build a dynamic, risk-based approach to fraud prevention and compliance. Accurately score customer risk in real-time, reduce false positives, and apply onboarding friction only when it matters.

How it works

Set the logic. Risk-profile the customer and transactions. Trigger the next steps.

Step 1

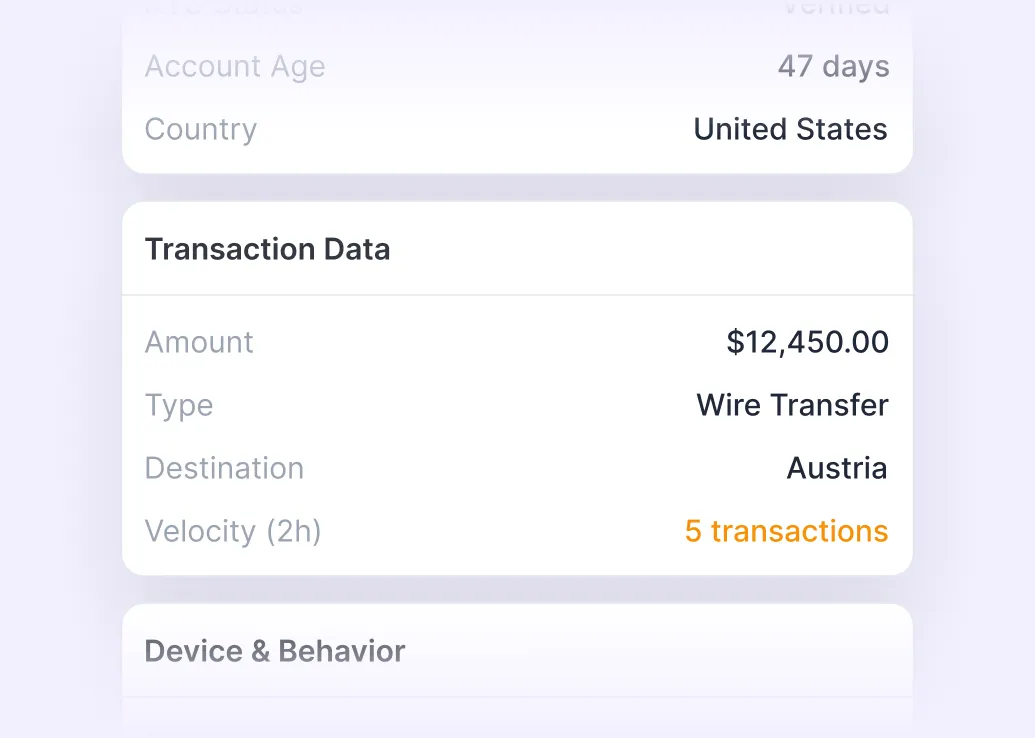

Collect contextual data

Pull in the information used to assess the customer profile and transaction details.

Step 2

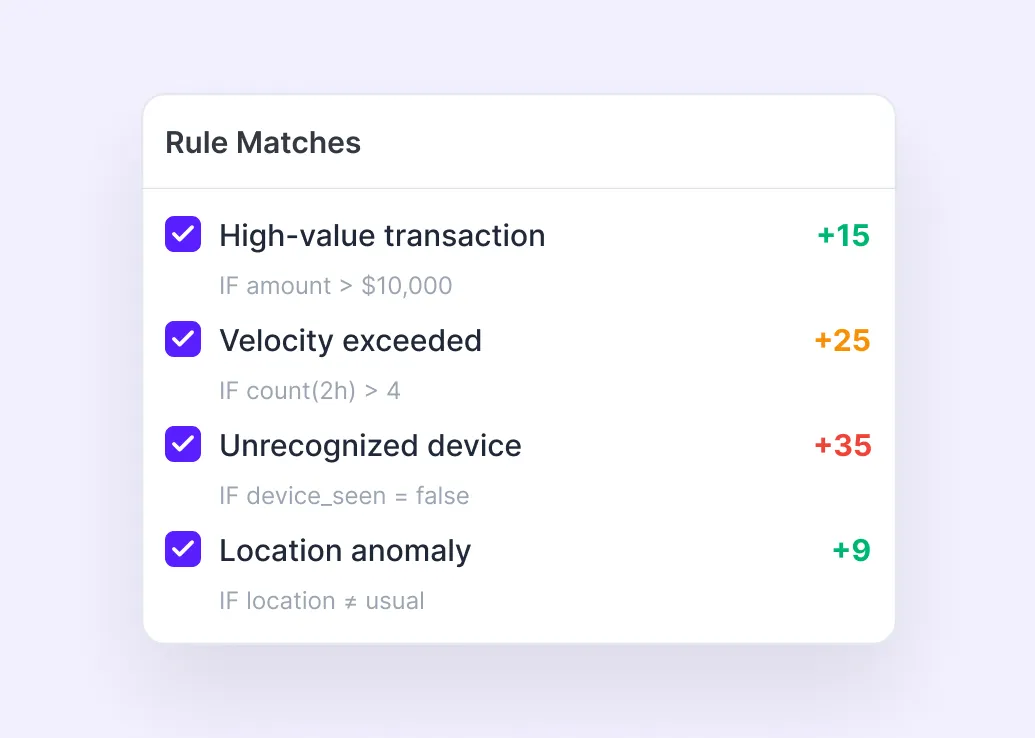

Apply risk rules

Assign points based on the factors that match the customer / transaction.

Step 3

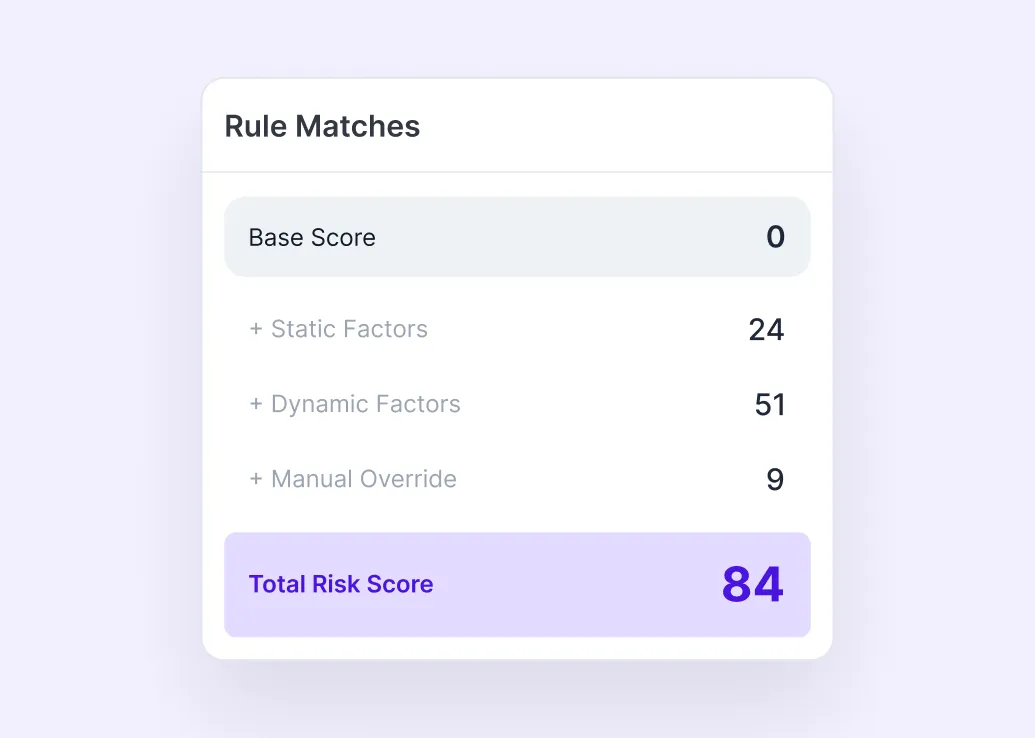

Calculate total risk

Combine static, dynamic, and manual factors into one score.

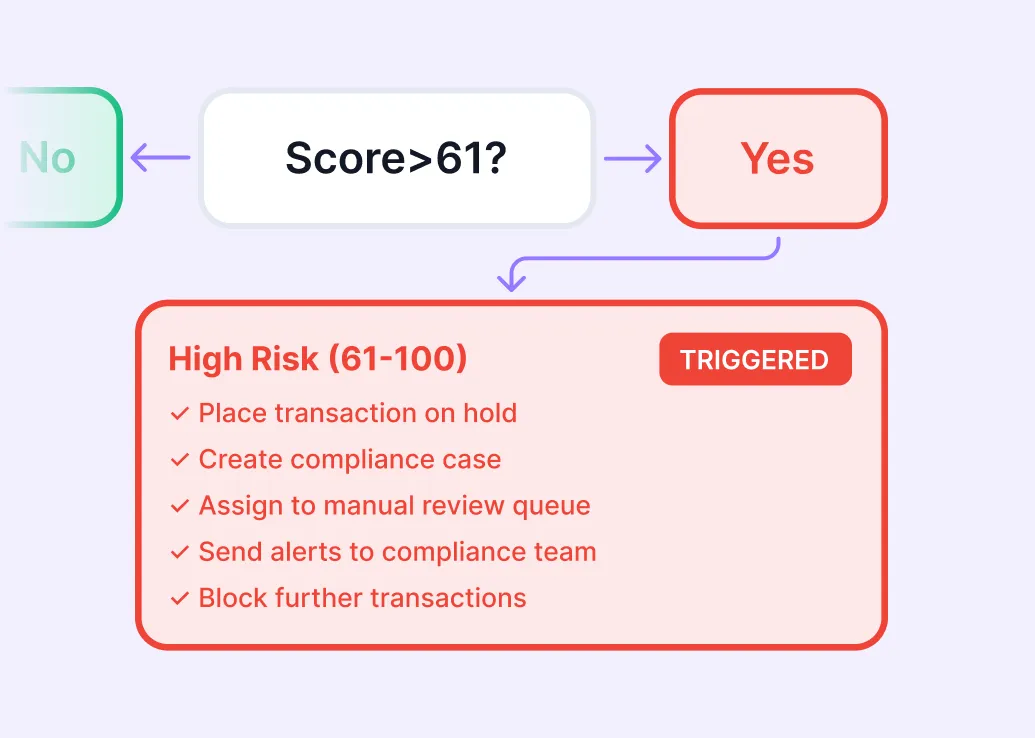

Step 4

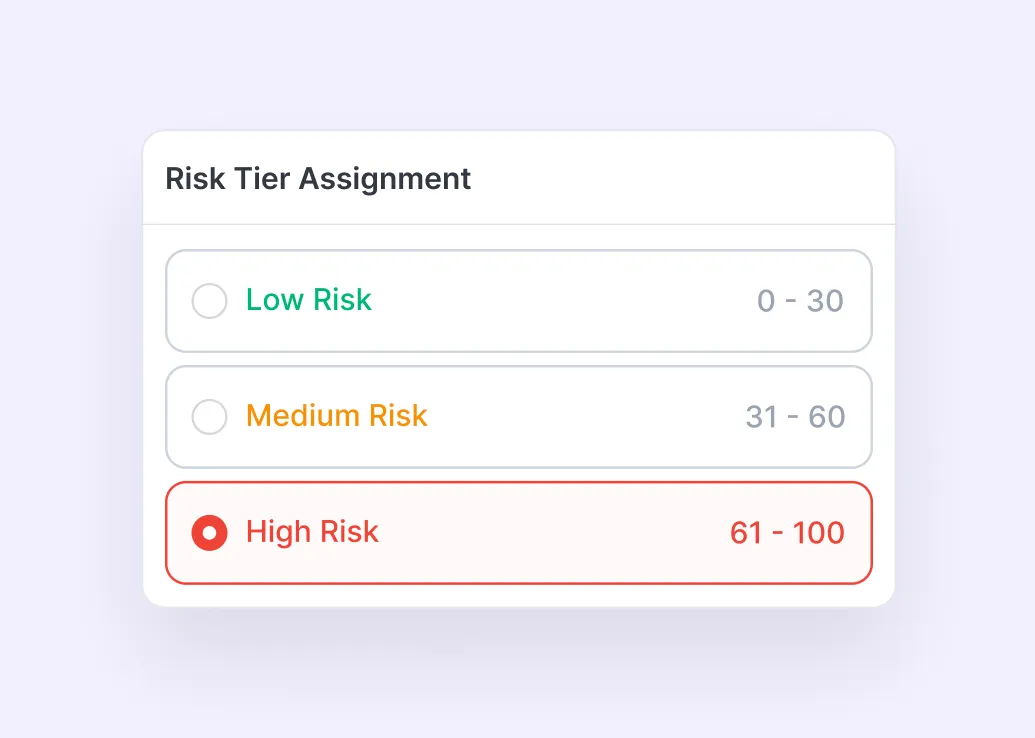

Assign a risk level

Place the customer into the relevant tier based on your thresholds.

Step 5

Trigger action

Route the case into approval, review, EDD, or monitoring

Risk Assessment Model

The factors behind each customer risk score

Velocity

Flags customers whose transaction activity spikes too quickly within a short time window, such as multiple deposits or outbound transactions in an hour.

Structuring

Detects patterns where larger sums may be intentionally split into smaller transactions over a short period of time to avoid thresholds, reporting requirements, or additional review.

Behavioral

Covers activity that does not fit a customer’s normal pattern, such as dormant account reactivation, sudden volume changes, and similar anomalies.

KYC/AML

Focuses on risks connected to sanctions, PEPs, criminal lists, adverse media, high-risk industries, and other customer or beneficiary AML concerns.

Technical

Captures suspicious technical signals such as proxy or Tor usage, impossible travel, attacker-linked IPs, and unusual login or access patterns.

Transfer

Monitors how funds move between senders and beneficiaries, including repeated transfers, frequent third-party funding, and high outbound volumes.

Profile

Flags transactions that appear inconsistent with the customer’s usual financial profile, balance behavior, supported currencies, or assigned risk factors.

Fraud

Looks for behavior often associated with fraud, such as device changes, bot or emulator use, dormant-account abuse, and suspicious device-switching before transfers.

Country exposure

Flags transactions connected to unexpected, high-risk, or sanctioned jurisdictions that may require closer review or stronger compliance controls.

Device

Detects risky device behavior, including one device being used by multiple customers or a single customer using multiple devices in a short period.

Regulatory

Covers mandatory compliance triggers such as Travel Rule data gaps, high cumulative risk, overdue AML re-screening, and mandatory reporting thresholds.

Industry risk

Evaluates the customer’s business sector to help determine whether it falls within low-risk, high-risk, or prohibited industry categories over time.

Outcome

Use risk scores to shape the customer journey

Apply review effort where it matters and keep lower-risk cases moving.

Common Use Cases

Where Risk Assessment creates the most value

Use automated risk scoring to route customers, trigger reviews, and support more proportionate compliance across industries.

Customer onboarding

Score users during onboarding to decide whether they can proceed through standard review, require enhanced due diligence, or need manual investigation.

Business onboarding

Assess legal entities using country, industry, structure, ownership, and PEP-related indicators before approval. This fits especially well with your KYB positioning.

Crypto and VASP compliance

Apply stronger scrutiny to customers, jurisdictions, and behaviors that carry elevated regulatory or fraud exposure. This aligns well with how risk scoring is commonly positioned for crypto compliance.

Ongoing AML Monitoring

Re-score customers when new transaction or behavioral anomalies appear and support continuous risk evaluation.

EDD triggering

Automatically identify high-risk profiles and escalate them into enhanced due diligence or human review.

Want to see it in your industry?

Benefits

Why businesses choose Identomat for Risk Assessment

Identomat helps businesses assess customer risk more intelligently, apply the right level of due diligence, and keep risk decisions consistent across the customer lifecycle.

Make better risk decisions with Identomat

Identomat helps businesses assess customers using multiple risk signals instead of relying on one-dimensional checks or fragmented manual reviews.

Support a risk-based compliance approach

With Identomat, businesses can apply proportionate due diligence based on actual customer risk and route cases more confidently into standard review, EDD, or manual investigation.

Reduce manual work for compliance teams

Identomat automates scoring logic and ongoing evaluation, helping teams spend less time on repetitive assessments and more time on cases that require attention.

Keep customer risk profiles up to date

Identomat makes it easier to update risk levels as new data, behavioral signals, or suspicious indicators appear over time.

Build around your own compliance framework

Identomat’s configurable risk logic helps businesses reflect their own policies, thresholds, and internal risk appetite instead of forcing a fixed model.

Create a more explainable review process

Identomat helps compliance teams understand what contributed to a customer’s risk score, making decisions easier to review, justify, and audit.

Security & Compliance

Built for secure, auditable compliance operations

Deploy Risk Assessment as part of a broader compliance infrastructure backed by recognized security standards and configurable controls.

FAQ

Frequently asked questions

Everything you need to know about the product and billing.

What information is typically used to assess a customer’s risk level?

A customer risk score is usually built from a mix of contextual and behavioral data, not just one check. On Identomat’s page, that includes factors such as KYC/AML signals, country exposure, device behavior, transaction velocity, structuring patterns, fraud indicators, profile consistency, and industry risk. More broadly, regulatory guidance also points firms to consider customer type, products and services used, geography, and expected account activity when building a customer risk profile.

Can one red flag automatically determine the final risk score?

Not by itself, at least not in a sound risk-based model. Identomat describes the score as a combination of static, dynamic, and manual factors, and FFIEC guidance similarly says firms should analyze all pertinent information and not treat any single indicator as automatically determinative of low or high risk.

Can different risk factors be weighted differently?

Yes. A practical risk model does not have to treat every signal equally. FFIEC guidance explicitly notes that some factors may be weighted more heavily than others depending on the institution’s risk profile, while Identomat’s page also emphasizes configurable logic, thresholds, and policies rather than a fixed one-size-fits-all model.

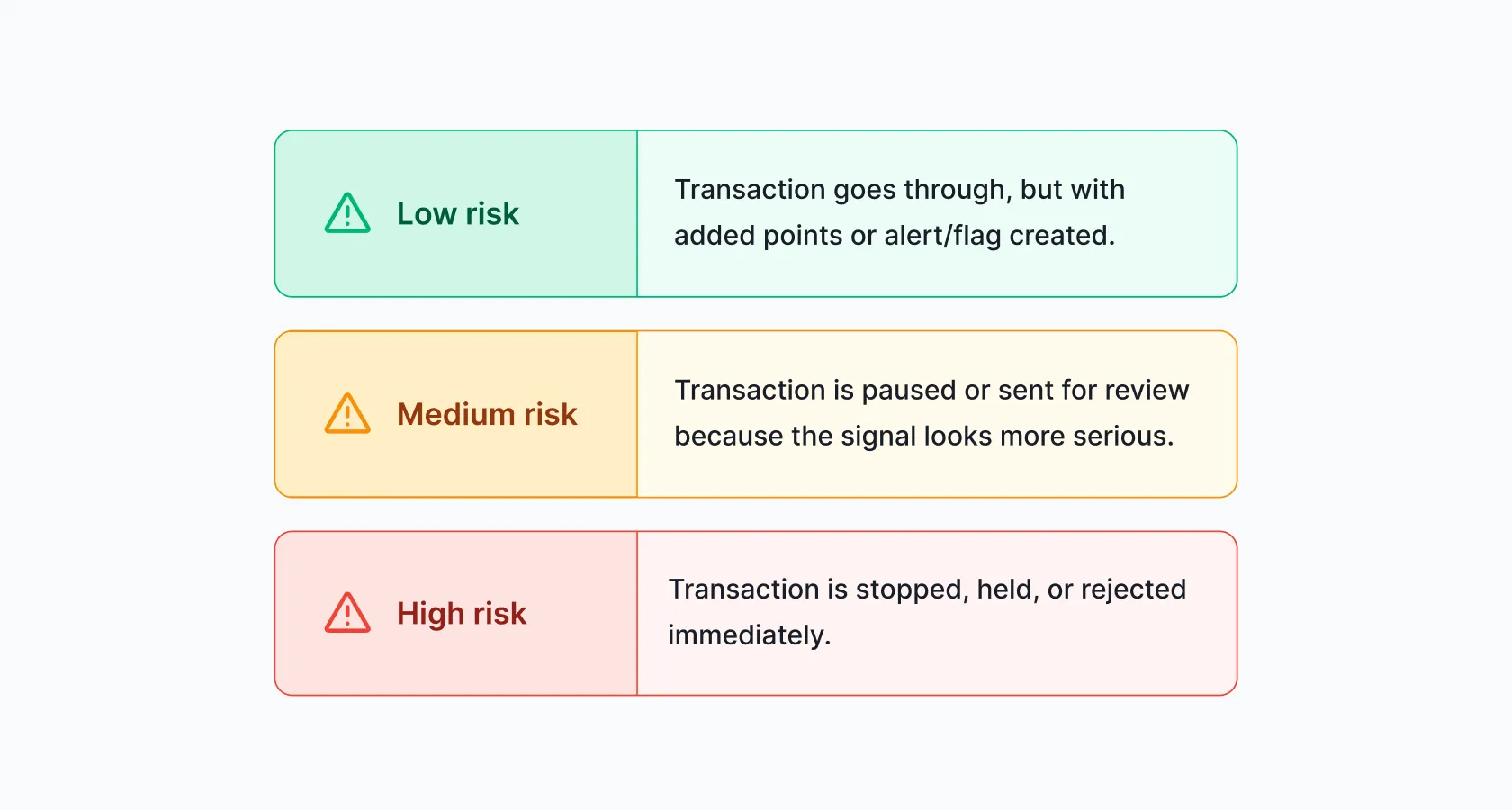

Do all higher-risk customers need the same treatment?

No. A risk-based approach is supposed to be proportionate, not blunt. FATF says higher risks should trigger enhanced measures, while lower risks may justify simplified or lesser measures where appropriate. That lines up with Identomat’s positioning of routing customers into different paths such as standard review, enhanced due diligence, manual review, or ongoing monitoring based on score and thresholds.

How often should a customer risk profile be reviewed or updated?

It should be updated when the customer’s risk picture changes, such as new products, new geographies, new customer segments, new transaction behavior, or other relevant signals. FFIEC guidance says risk assessments are generally updated to reflect changes in products, services, customers, and geographies, though there is no universal requirement to refresh them on one fixed schedule. Identomat’s page also frames risk assessment as something that stays current as new data and suspicious indicators appear over time.

Why does explainability matter in a risk assessment process?

Because compliance teams need to understand and justify why a customer was scored a certain way. FFIEC describes written documentation as a sound practice for communicating risks and the factors behind them, while Identomat highlights explainable reviews as important for auditability and internal justification. In other words, “the algorithm felt moody” is not a compliance framework.

Risk-based compliance starts here

Create a risk scoring flow with Identomat that matches your business model, risk logic, and compliance requirements.