These last couple of years blockchain technology has witnessed extensive progress in terms of acceptance by the authorities. In particular, crypto companies are now conditioned as conventional Financial Institutions when it comes to Anti-Money Laundering and KYC laws and regulations. One major field that doesn't fall into the traditional asset exchange category but is being increasingly hit in such circumstances is DeFi.

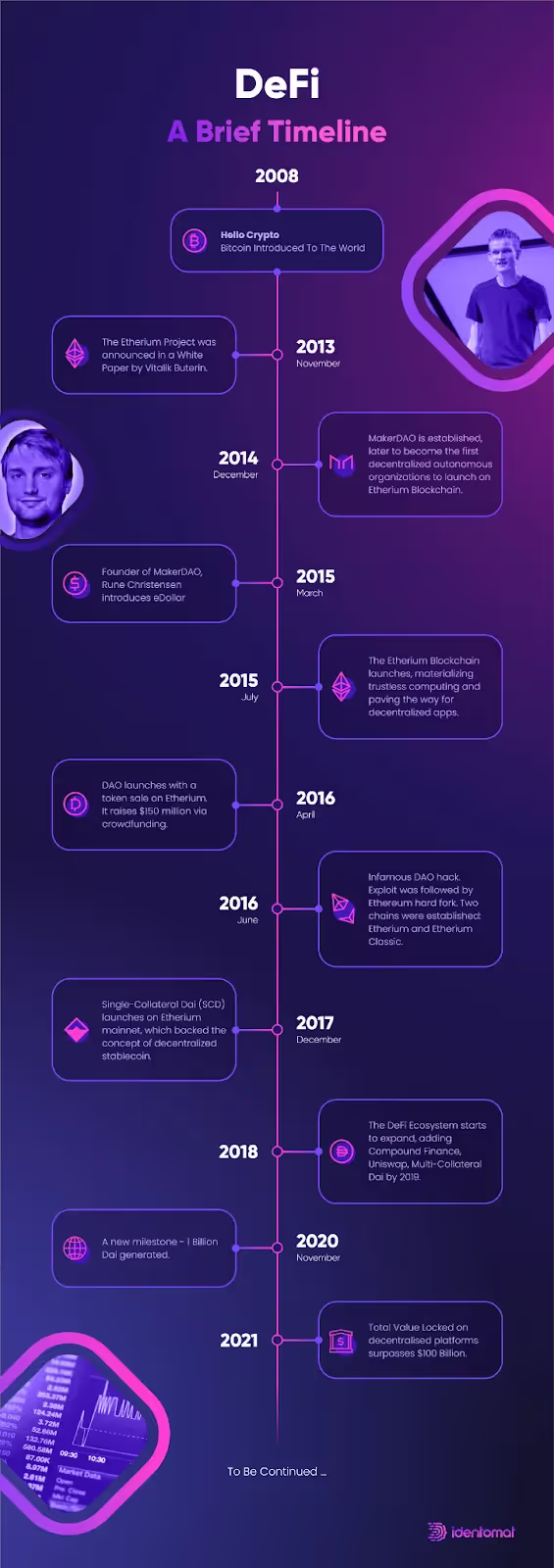

Before we dive into it, let’s specify the meaning behind DeFi; It is short for Decentralized Finance and signifies that cryptocurrency entrepreneurs are able to at minimum recreate traditional financial instruments in a decentralized architecture, outside of companies’ and governments’ control. DeFi’s potential and breadth of use cases go way beyond CeFi (centralized finance), the topic which we will try to cover in the near future. Before that, let’s take a quick look at a brief history of DeFi:

What does the new outlook mean for DeFi

Nowadays, data security and compliance with emerging regulations means that you, as a company, are sober to potential risks coming your way. Taking purposeful actions to contain the risks, puts you on the good side of the law. This positioning also opens room to attracting institutional and/or corporate customers, who are adamant about safeguarding themselves and their data. Demonstrating that you are following with KYC and AML compliance regulations can be used to expand your customer base.

DeFi has managed to augment automated market making and liquidity pooling through massive decentralization and very clever algorithms, but if it wants to match CeFi’s fraud prevention and security levels, its community needs to adopt AML measures.

- David Lomiashvili, CEO of Identomat.

"DeFi is all about taking the middleman out of financial transactions. As much as decentralized, open markets with efficient capital turnaround and higher average yields are enticing, they come at a significant cost to market security. Let us not forget that traditional financial organizations that act as middleman play an important role in mitigating these risks. DeFi has managed to augment automated market making and liquidity pooling through massive decentralization and very clever algorithms, but if it wants to match CeFi’s fraud prevention and security levels, its community needs to adopt AML measures. I don’t expect this to happen, though, until we have similarly decentralized KYC solutions that live up to the values of DeFi community – creating censorship-proof open markets that foster true financial inclusion. That is why Identomat is working hard with our partners to kickstart this next chapter in the unstoppable DeFi revolution. " - Says David Lomiashvili, CEO of Identomat.

Expert takes on DeFi’s potential vary significantly, however, the consensus seems to be that it is realistic to expect traditional financial markets be eventually overtaken by decentralized ones, given that government regulations are complied with. Whether DeFi breaks into larger markets (shown on the chart below) and eventually approaches $400 trillion global financial market, depends on the level of adoption of financial and security regulations including KYC/AML.

KYC shouldn’t automatically be interpreted as centralization. A DeFi app can facilitate decentralized financial transactions and simultaneously give access to verified users.

Pitfalls of mass adoption of unregulated DeFi

Since DeFi platforms are expanding their use horizons, the FATF has an unyielding determination to disallow further operations of exchanges and DeFi platforms without KYC.

According to CipherTrace report notable DeFi hacks in 2020 included:

- bZx

- Akropolis

- Axion Network

- Balancer

- Bancor DEX

- Bisq

- Cheese Bank

- COVER

- Finance

- Harvest Finance

- Lendf.Me

- Opyn

- OUSD

- Pickle Finance

- Uniswap

- Value DeFi

- WarpFinance

- wLEO

The same research states that "the exponential explosion of capital and lack of regulatory clarity have attracted criminal actors to DeFi, ultimately resulting in the most DeFi hacks in a year to date". To put this statement into numbers, there was $516 million in 2020 thefts, DeFi added $129 million to crypto thefts.

The above example alone is enough to state that the field will not be able to reach commercial and legal sustainability sans KYC and AML protocols.

But the problem lies with the ‘D’ - standing for ‘Decentralized’, which, in first, was the most attractive part for many. So, who or what can regulate a concept that in its core, shouldn’t be regulated?

Bad Blood: Can DeFi and KYC cooperate?

One of the main components of DeFi has been anonymity. The complication here is that FATF has made it clear that undisclosed financial transactions open a window to criminal exploitation. Therefore, treating owners/users of a DeFi app as Virtual Asset Service Providers (VASPs) would be the way-out. This directly means that DeFi platforms will have to put into operation the KYC process or otherwise be confronted by regulatory sanctions.

Now, DeFi owners and users are facing a tough decision whether to take in KYC standards or decide how important being compliant to the regulation is at all - which may lead to a divide: DeFi that is regulated, compliant, transparent and more reliable and DeFi that is anonymous and, therefore, unregulated. The bottom line is, that at some point, DeFi will have to accept the neglect from a part of its target market.

Identomat is working hard with our partners to kickstart this next chapter in the unstoppable DeFi revolution.

- David Lomiashvili, CEO of Identomat.

Ultimately, the process should be directed in favor of regulations if DeFi platforms wish to stay active and engaged with the bigger financial market.

Ready to get started?

Empower your platform with Identomat's cutting-edge KYC and AML ID verification.

Book a demo

Frequently asked questions

What are the risks of operating a DeFi platform without KYC?

Unregulated DeFi platforms face significant risks, including fraud, hacks, theft, regulatory sanctions, and exclusion from major markets. CipherTrace reported millions lost in DeFi hacks, and regulators have signaled that platforms without AML/KYC controls will face restrictions or shutdowns.

Why are global regulators pushing for KYC in DeFi?

Agencies like the FATF and EU regulators want to prevent money laundering, terrorism financing, and anonymous financial abuse. Since DeFi transactions often move large amounts of capital rapidly, KYC ensures transparency and protects both users and markets from criminal exploitation.

How can DeFi projects implement KYC without harming the user experience?

By using automated verification tools like Identomat, ID checks are completed in seconds. DeFi users can verify once and transact securely, while platforms maintain a fast and seamless onboarding flow - essential for retaining users in a high-speed market.